Business Survival - Insurance Price Survival Kit

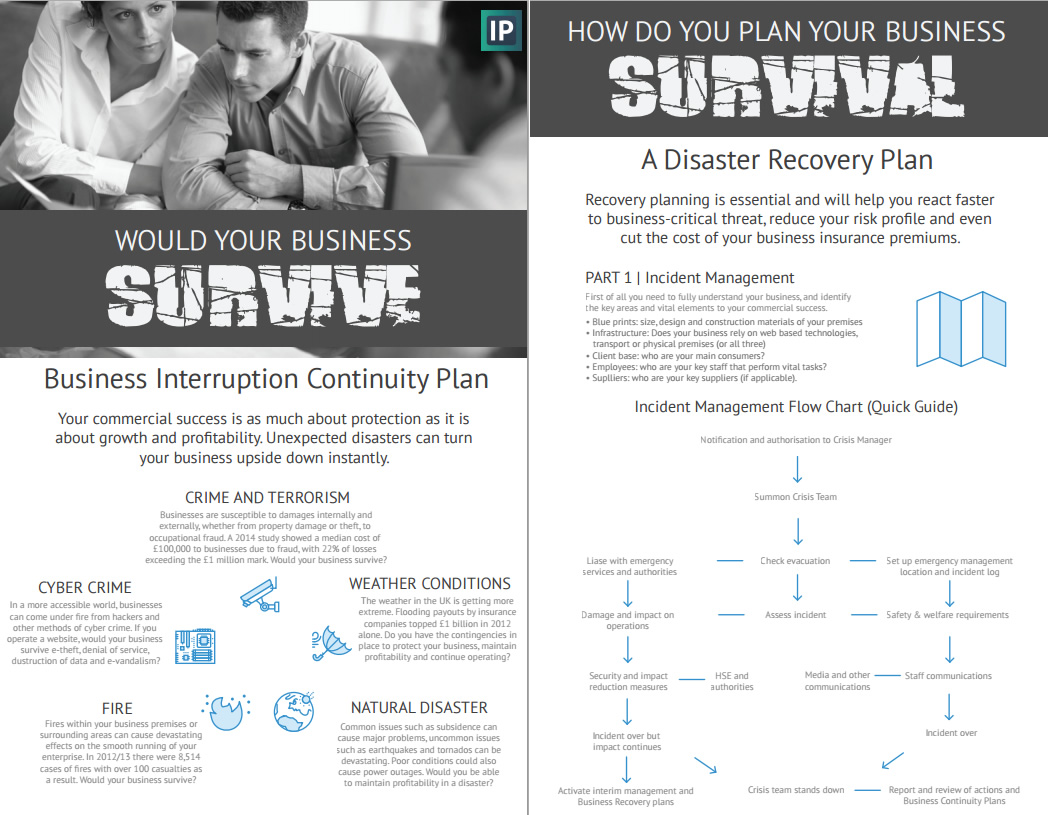

Your commercial success is as much about protection as it is about growth and profitability. Unexpected disasters can turn your business upside down instantly.

For easier reference, and examples of a continuity and crisis management flow chart, please download our Business Survival kit below.

Business Interruption Causes

Crime and Terrorism

Businesses are susceptible to damages internally and externally, whether from property damage or theft, to occupational fraud. A 2014 study showed a median cost of £100,000 to businesses due to fraud, with 22% of losses exceeding the £1 million mark. Would your business survive?

Cyber Crime

In a more accessible world, businesses can come under fire from hackers and other methods of cyber crime. If you operate a website, would your business survive e-theft, denial of service, destruction of data and e-vandalism?

Fire

Fires within your business premises or surrounding areas can cause devastating effects on the smooth running of your enterprise. In 2012/13 there were 8,514 cases of fires with over 100 casualties as a result. Would your business survive?

Weather Conditions

The weather in the UK is getting more extreme. Flooding payouts by insurance companies topped £1 billion in 2012 alone. Do you have the contingencies in place to protect your business, maintain profitability and continue operating?

Natural Disaster

Common issues such as subsidence can cause major problems, uncommon issues such as earthquakes and tornados can be devastating. Poor conditions could also cause power outages. Would you be able to maintain profitability in a disaster?

How To Plan Your Business Survival

Recovery planning is essential and will help you react faster to business-critical threat, reduce your risk profile and even cut the cost of your business insurance premiums.

PART 1 | Incident Management

First of all you need to fully understand your business, and identify the key areas and vital elements to your commercial success.

- Blue prints: size, design and construction materials of your premises

- Infrastructure: Does your business rely on web based technologies, transport or physical premises (or all three)

- Client base: who are your main consumers?

- Employees: who are your key staff that perform vital tasks?

- Suplliers: who are your key suppliers (if applicable).

PART 2 | Risk Assessment

Given the outlined threats to your business, evaluate and measure the risk to each critical element, considering:

- Maximum period of failure or downtime the business can sustain.

- The likelihood of danger or failure to critical business elements.

- The impact on gross profit or gross fees should a disaster occur.

- The worst case scenario.

- Impact on employees and clients.

PART 3 | Ensure You Have The Correct Cover

It is critical that you have the right cover. The primary role of business interruption insurance is to protect your enterprise against loss of gross profit or to cover your gross fees for reduction in turnover as a result of an insured claim. Once you understand your business needs and have a continuity plan in place, you will have a better idea of how much cover you will need. We have outlined below the indemnity period that types of businesses should be aiming for.

What Indemnity Period

12-18 Months

Simple retail or office based with no or modest special internal specifications. For firms that can easily re-locate to new premises as they do not own the premises they occupy. Not for manufacturers, operations with complicated internal kit arrangements or firms in green belt areas where planning permission will be complex.

24 Months

Complex retail or office and simple manufacturing or infrastructure plants. For organisations with complicated internal specification requirements or affected by green belt issues. Good for manufacturers with simple processes and without key plant to be sourced, delivered and commissioned. Not for manufacturers with complicated processes or key plant that is difficult to source.

36 Months

For firms that lease property to third parties - whether individuals or organisations - on a loss of rent receivable insured basis. Also for manufacturers and supply chain businesses with complicated processes where key plant or assets are neither readily available nor replaceable.

In summary, you may need more than 36 months so don’t be afraid to ask for longer indemnity periods. Always build in slack, it can take longer than you think to recover. Ensure your indemnity period gives you the time and flexibility to re-launch your business confidently.